Abstract

The Web3 social platform Friend.Tech, launched in August 2023, enables users to tokenize and trade their social influence. While attracting 139K users, Friend.Tech's economic model and business strategy face significant challenges. After collecting and analyzing relevant on-chain data, we find that the platform's economic model generates early substantial returns for key opinion leaders but also restricts community size and stable profit potential, with 99.4 percent of accounts having fewer than 100 followers. Numerous speculative users are attracted to the platform, but only 22.1 percent of speculative returns are positive, and the trading frequency rapidly declines, with the average token holding period exceeding 4 days. The reliance on new users, combined with an inevitable decline in platform activity, indicates a less optimistic outlook for the sustainability of this economic model. The platform demonstrates a high level of transitivity and tighter social connections compared to existing social platforms. In conclusion, while Friend.Tech appears economically unsustainable, its social model shows promising prospects and serves as a valuable exploration and demonstration for the development of Web3.

What is FRIEND.TECH?

The Latest Work from a Pioneer of the SocialFi Model

Following DeFi (Decentralized Finance) and GameFi (Game Finance), SocialFi (Social Finance) has become one of the hottest concepts in the Web3 space. This model combines decentralized financial services with social media, offering users a new way to derive economic value directly from social interactions and content creation.

After developing two popular Web3 social applications—TwitterDAO and Stealcam—developer Racer launched Friend.Tech on August 10, 2023. Built on the SocialFi model, this blockchain-based social platform allows users to trade cryptocurrency for the right to engage in private one-on-one chats with other users.

This app, which directly links social influence with economic value, is especially appealing to crypto enthusiasts—it offers regular users direct access to influential KOLs (Key Opinion Leaders), while also providing KOLs with a new avenue to monetize their influence.

Friend.Tech Links Influence Value with Economic Value

Friend.Tech Gameplay:

- Users connect their Twitter (X) accounts within the app; each account corresponds to a set of Keys (initially called Shares), with no upper limit on the number of Keys per account.

- Each Key set starts at zero, and users can claim their first Key for free to activate further functionality.

- Users can purchase Keys from others to become Holders, thereby gaining the right to engage in one-on-one private conversations with that user.

- Users can buy multiple Keys from various users (including themselves) and sell previously held Keys back to the platform.

Friend.Tech operates on the Base chain (an Ethereum Layer 2 network). Holder lists (wallet addresses on the Base chain) and Key quantities are stored in smart contracts, and transactions are conducted using ETH. A Friend.Tech account must be linked to a Twitter (X) account to obtain a blockchain address. However, due to the openness of smart contracts, users can generate addresses and interact with the contract without entering the app interface. We refer to all such addresses as "users" for simplicity.

Figure 1 - Application Interface

Figure 1 - Application InterfaceTokenomics · Token Economy Concept and Analysis

A Rigid Economic Model

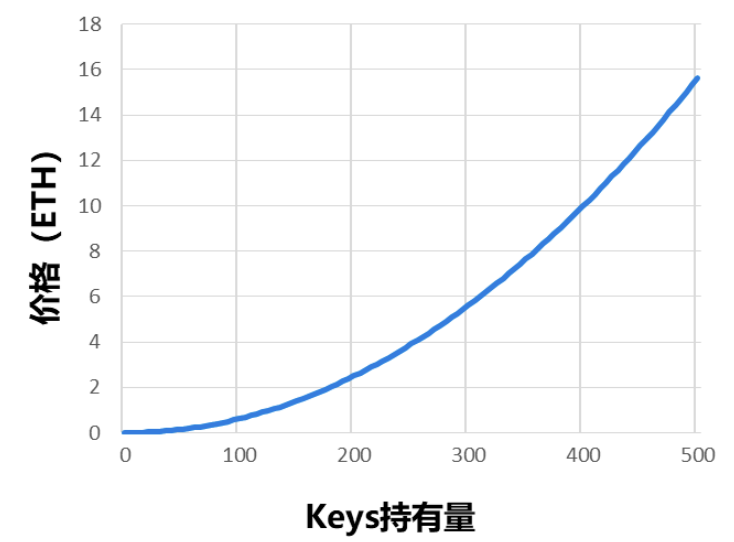

Keys do not follow traditional order-book or AMM (Automated Market Maker)-based pricing mechanisms commonly used in decentralized exchanges. Instead, they use a fixed price formula based on the total quantity currently held on the platform.

Figure 2 - The Relationship Between Keys Holdings and Price (ETH)

Figure 2 - The Relationship Between Keys Holdings and Price (ETH)Buying Price (in ETH):

Price = (previous holding amount)^2 / 16000Selling Price (in ETH):

Price = (holding amount before sale - 1)^2 / 16000

In practice, when purchasing Keys:

- An additional 10% fee is charged:

- 5% goes to the creator of the Keys

- 5% goes to the Friend.Tech project team for development, support, and community building

When selling Keys:

- Only 90% of the proceeds are returned to the seller:

- Again, 5% goes to the creator

- 5% to Friend.Tech

This means that if a user sells a Key at the same price it was bought, they incur a 20% fee loss. These two 5% fees are collectively referred to as protocol revenue below.

Although the notional price of Keys increases quadratically with the number held:

- Holding increases by 1 → value increase =

2 * previous holdings / 16000 - Holding increases by N → value increase =

(2 * n * previous holdings + n^2) / 16000

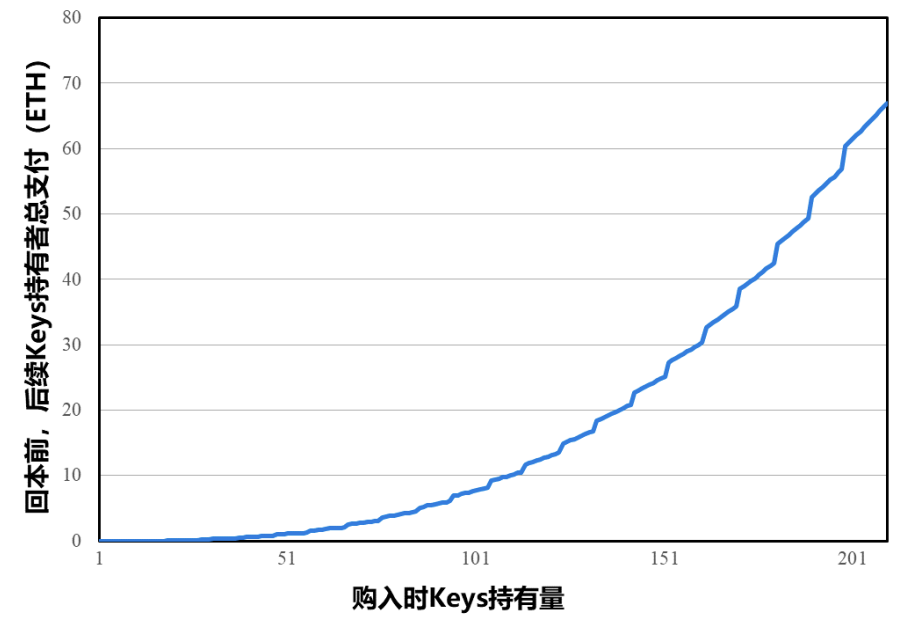

Due to the fee structure, even with increased holdings, selling does not necessarily yield profit. In fact, the number of Keys held needs to increase by approximately 10.6% just to break even. Before that, the cumulative cost grows exponentially. For example, if a user buys the 200th share of a Key, they would need subsequent buyers to purchase 22 more Keys (a total of 68 ETH spent) to break even upon resale.

Figure 3 - The amount of subsequent user payments required to achieve a paper profit after purchasing Keys at different times.

Figure 3 - The amount of subsequent user payments required to achieve a paper profit after purchasing Keys at different times.The rigid economic model clearly presents both strengths and weaknesses.

We offer the following analysis and assumptions about this model, supported by on-chain data verification.

Data Source: On-chain data from the Friend.Tech smart contract (0xcf20) on Base chain. As of September 19, there were 6,456,148 transactions involving the contract, of which 3,049,066 were related to buying/selling Keys.

Advantages of the Economic Model:

- Avoids initial low liquidity and price volatility during cold start. The bid-ask spread encourages holders to promote Keys actively—profitability depends on continued growth in holdings, aiding early-stage adoption success (see Section 3.1).

- Direct access to KOLs has real value, allowing early investors to identify promising creators (see Section 3.3).

- KOLs benefit significantly from the value of one-on-one interaction (see Section 3.4).

- High costs of late-stage speculation (including time and opportunity costs) reduce the likelihood of infinite price inflation (see Section 3.4).

Potential Issues with the Economic Model:

- Encourages speculative behavior. Since prices only go up, early adopters and bots dominate (see Section 3.3).

- Limited intrinsic value of one-on-one chats leads to capped demand. Rational fans won’t pay premium prices once the novelty wears off (see Section 3.4).

- Rapid decline in activity after early hype. Once early sellers exit, high-cost holders struggle to find buyers (see Section 3.5).

- Platform growth depends on constant influx of new KOLs. Without them, trading stagnates (see Section 3.5).

Finally, we explore a core question at the end of this report:

Does the project truly foster social interaction? (See Section 3.6)

Tokenomics · On-Chain Data Evidence

3.1 – First-Month Performance Test

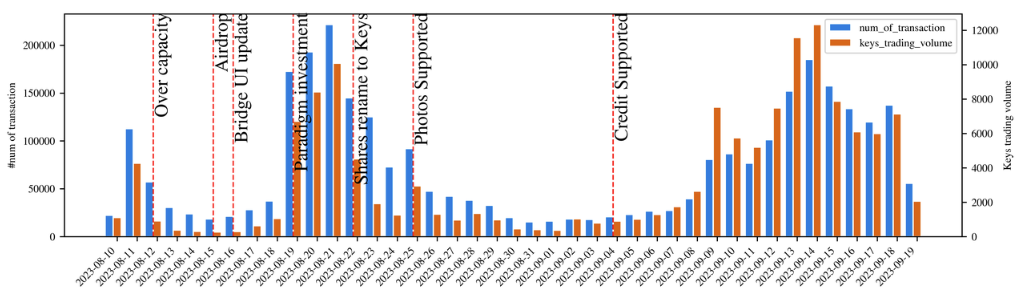

Despite being in a six-month test phase, Friend.Tech saw immediate success. It launched on August 10, and recorded:

- 17,556 Keys created

- 136,000 daily transactions

- Over 4,000 ETH traded on August 11 alone

On August 19, Paradigm, a top-tier Web3 VC, announced seed funding, sparking another surge. On August 21:

- Over 10,000 ETH traded

- 525,000 transactions

- Daily protocol revenue exceeded 500 ETH—higher than major chains like Tron and Uniswap

From August 10 to September 19:

- 206,706 users

- 203,953 Keys created

- 258,859 Keys held

- 3,049,066 transactions

- Total volume: 139,530.09 ETH

Figure 4 - Project Daily Transaction Count and Trading Volume (as of September 19, 2023)

Figure 4 - Project Daily Transaction Count and Trading Volume (as of September 19, 2023)For a social networking project, attracting nearly 140,000 users in one month (regardless of engagement level) demonstrates significant growth potential and profitability for SocialFi applications.

3.2 – Three Main User Types

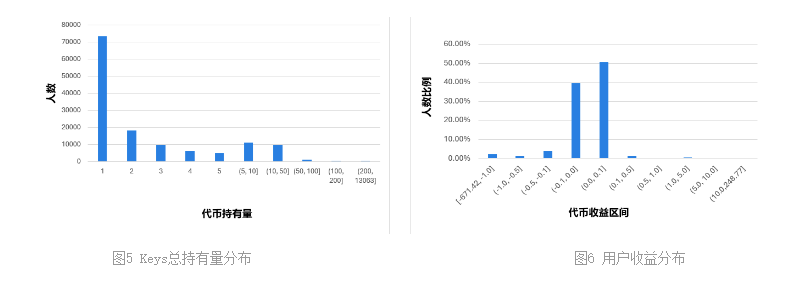

Most users have near-zero net profit/loss, but gains follow a long-tail distribution.

Overall:

- Most users hold only one Key

- A minority participate in additional trades (Figure 5)

- Excluding gas fees, 90.2% of users had profits/losses within ±0.1 ETH

- 52.6% achieved positive returns, but only 2.17% earned over 0.1 ETH

- Top 100 users earned 4,311.64 ETH, representing 47.9% of total earnings, despite accounting for less than 0.1% of users (Figure 6)

Earnings reflect realized PnL only—not unrealized gains/losses (e.g., unsold Keys).

Figure 5 - Distribution of Hold and Profit

Figure 5 - Distribution of Hold and ProfitWe classify users into three categories:

- Light Participants: Majority of users who lightly engage in social activity and try Keys trading occasionally, often motivated by celebrity fandom, narratives, or airdrop incentives.

- Crypto KOLs: They build community value and attract followers to buy Keys for exclusive access. We define 4,718 users with ≥0.1 ETH in protocol revenue and connected Twitter accounts as KOLs.

- Speculative Traders: Not active social participants but trade hot Keys aggressively for profit. Extreme traders may use bots. We define 44,843 users whose total transaction volume exceeds the volume of their own Keys' trades as speculators.

The latter two groups trade more frequently and may overlap (e.g., a KOL might also speculate). This report focuses on analyzing these two groups.

3.3 – Speculator Behavior and Earnings

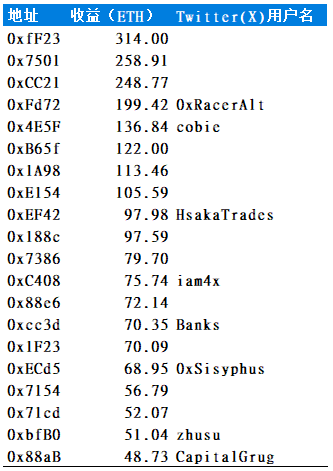

Among the top 20 highest-earning users are well-known figures like Cobie and Zhusu, along with many unverified users, indicating clear speculative activity.

Figure 6 - Top 20 Users by Total Earnings (ETH)

Figure 6 - Top 20 Users by Total Earnings (ETH)Of the top 100 earners:

- 65 are speculators

- 52 are KOLs

- 13 KOLs also speculate

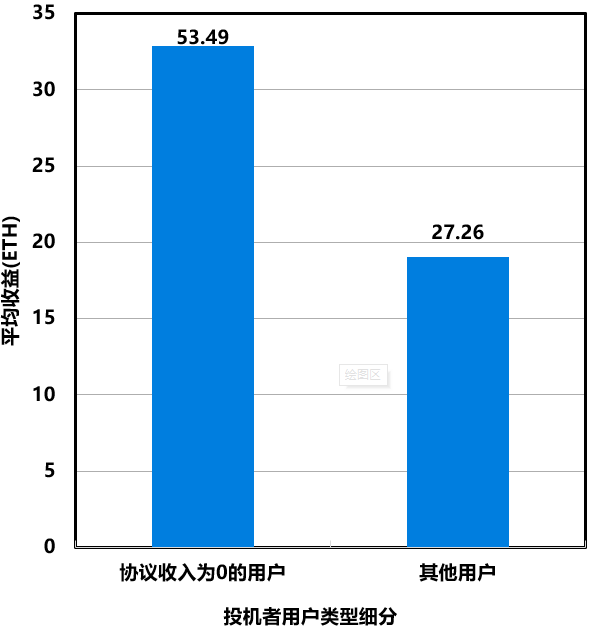

- 45 speculators earned zero protocol revenue

- Average speculator gain: 53.49 ETH

- Rest of top 100: 27.26 ETH (Figure 7)

Figure 7 - Comparison of Total Earnings Between Users with Zero Protocol Revenue and Other Users

Figure 7 - Comparison of Total Earnings Between Users with Zero Protocol Revenue and Other UsersSpeculators Drive Transaction Volume

- Represent 21.7% of users

- Account for 78.9% of total trades and 88.4% of total volume

- Only 28.8% of their trades involve KOLs, yet they contribute 82.5% of the value

- Platform vitality heavily relies on speculators, particularly those targeting KOL-created Keys

Speculation ≠ “Smart Money”

Only 8,346 (18.6%) speculators made positive returns. Of these:

- 900 (10.8%) did not bind social accounts

- Total smart money earnings: 5,443.32 ETH

- Non-social accounts contributed 60.9% of smart money returns

Approximately 186 Bot-Like Accounts

As Web3 teaches us, human efficiency pales next to bots. Friend.Tech bots monitor and instantly purchase cheap Keys upon creation or during rapid growth phases.

Within two weeks of launch:

- 186 MEV-like bots emerged

- Conducted 27,648 sniper trades

- Generated 463.21 ETH in volume

- Realized 2,553.84 ETH in profit—28.3% of total user profits

Figure 8 - Top 10 Suspected Bot User Transaction Volumes3.4 – KOL Behavior and Earnings

KOLs earn reliably through protocol revenue.

For most crypto users, the main draw of Friend.Tech is direct access to KOLs. Hence, early trades centered around KOL Keys, generating substantial income for KOLs.

- 86.5% of users received protocol revenue

- 4,718 users earned ≥0.1 ETH, totaling 93.2% of all protocol revenue

- Avg: 1.37 ETH

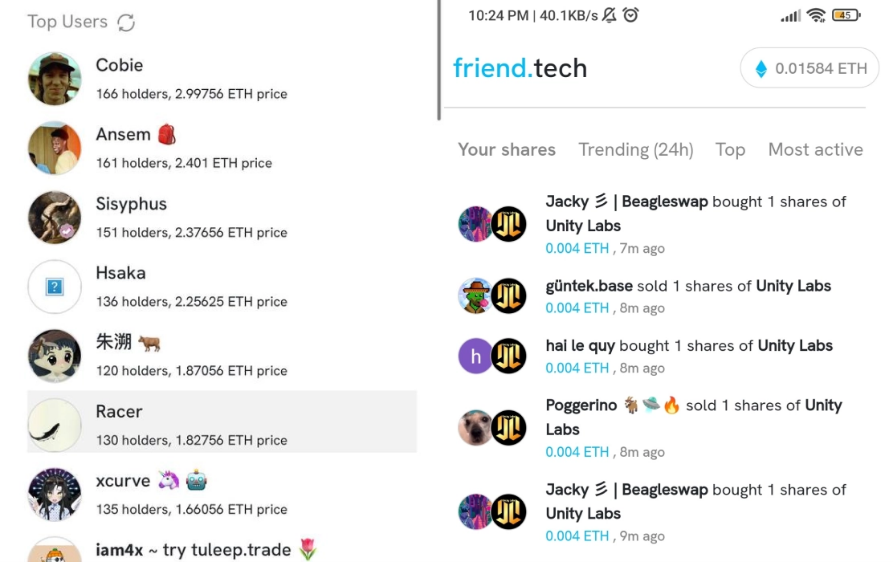

Top 3 KOLs:

- 0xRacerAlt: 202.57 ETH

- cobie: 139.19 ETH

- HsakaTrades: 134.18 ETH

Based on average ETH price from Aug 10–Sep 19, daily earnings ≈ $6,000–8,000 USD

Figure 9 - KOL Account

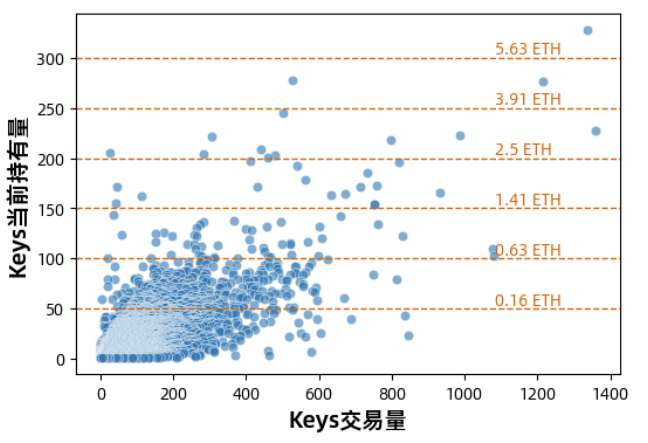

Figure 9 - KOL AccountHowever, a key observation is that most accounts hit a ceiling in Key holdings:

- 99.94% have <100 Keys (price <0.6 ETH)

- Even top KOLs rarely exceed 250 Keys (price <4 ETH) (Figure 9)

Figure 10 - Relationship Between Keys Trading Volume and Current Keys Holdings

Figure 10 - Relationship Between Keys Trading Volume and Current Keys HoldingsSelf-Buying Isn't Always Profitable

Some users believe in their social influence and adopt a strategy similar to bots—buying Keys early and selling high later. In reality:

- 18.9% of users employed this tactic

- 29.3% (11,493 users) profited, averaging 0.28 ETH

- Speculators had a higher success rate (18.6%) and higher average returns (0.65 ETH)

- Higher self-holding correlates with narrower profit margins—limiting upside but reducing downside risk

Among KOLs:

- 68.1% (3,211 users) bought their own Keys

- 535 engaged in arbitrage, earning avg 0.14 ETH (max 3.89 ETH)

- Top 3 KOLs (0xRacerAlt, cobie, HsakaTrades) largely avoided personal Key trading

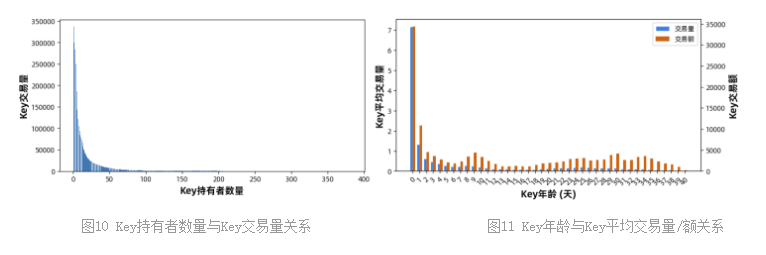

3.5 – Lack of Platform Sustainability

Figure 11 - Holders, Trading Volume and Key Age

Figure 11 - Holders, Trading Volume and Key AgeOn-chain data shows rising Key prices lead to reduced trading activity (Figure 10), declining almost exponentially. Similarly, older Keys see fewer daily trades and lower volumes (Figure 11). Trading peaks occur on the day of creation (avg 7/day), dropping to 2/day by Day 2, and rarely exceeding 1/day afterward—a result of the tokenomic design favoring early buyers.

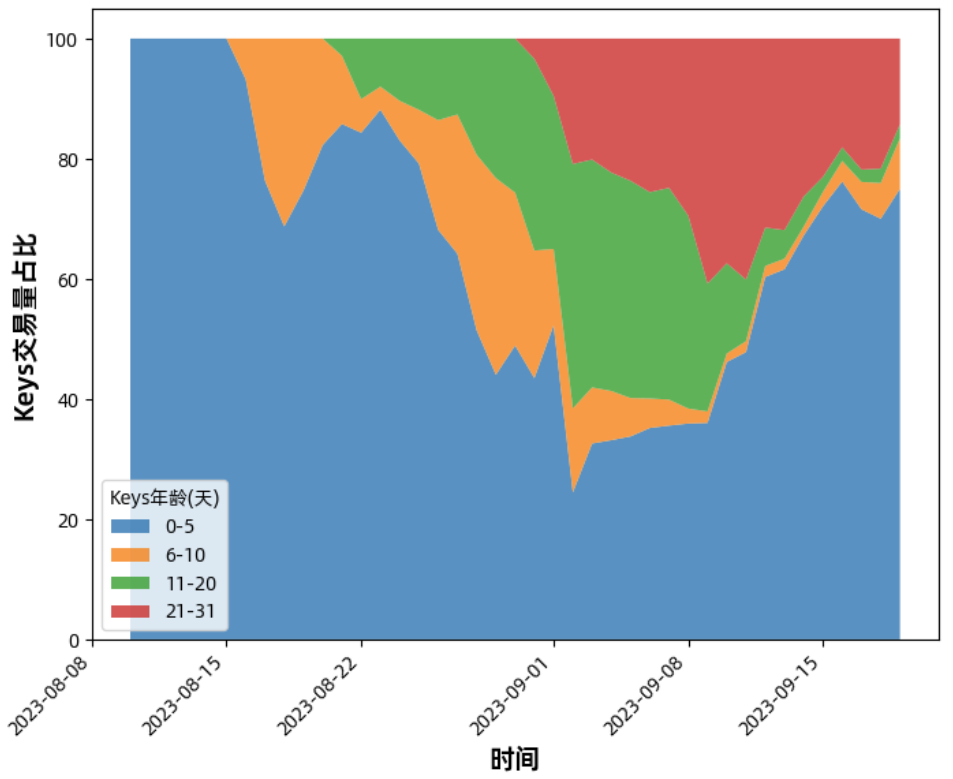

Figure 12 - Proportion of Keys Trading Volume by Keys Age Type Over Time

Figure 12 - Proportion of Keys Trading Volume by Keys Age Type Over TimeOne month post-launch, nearly half of daily trading still involves new Keys. If Friend.Tech struggles to attract new KOLs, trading volume will dwindle, threatening platform sustainability.

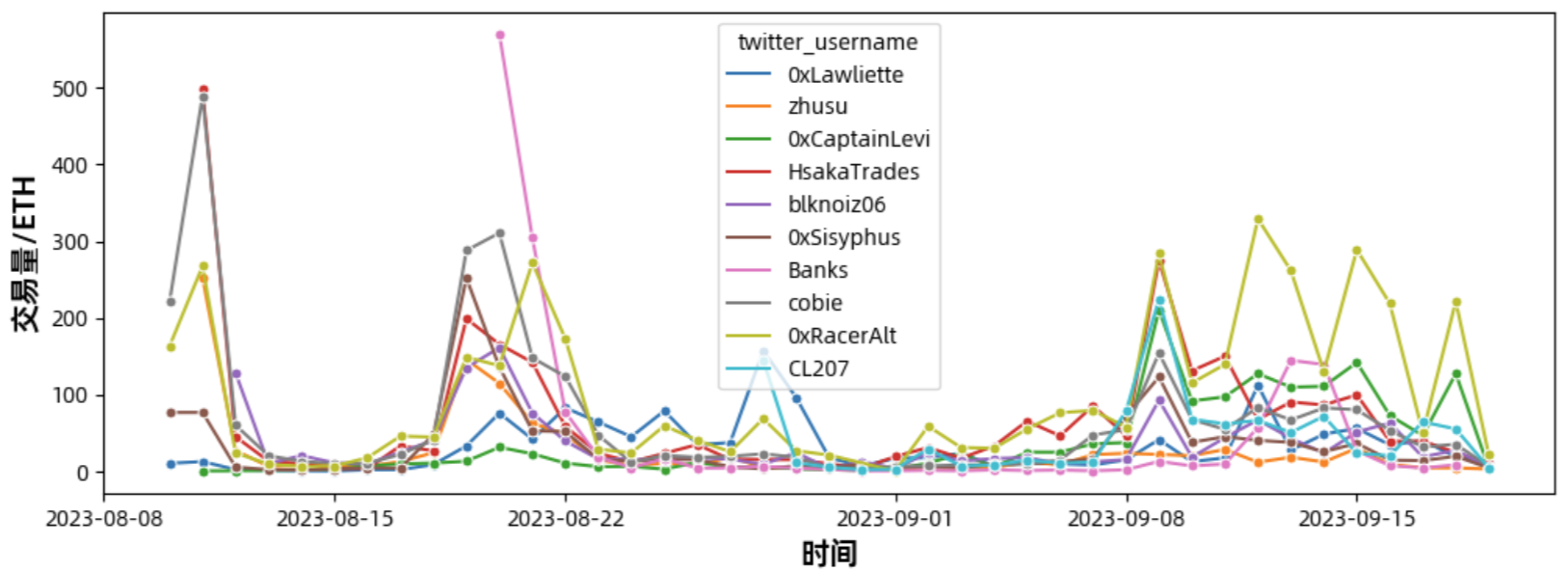

Figure 13 - Top KOLs' Keys Trading Volume Over Time

Figure 13 - Top KOLs' Keys Trading Volume Over TimeTop KOLs’ Keys historically sustained volume, but except for 0xRacerAlt and 0xCaptainLevi, most Top 10 KOLs show declining trends. If top KOLs fail to sustain interest, the project's longevity will be challenged.

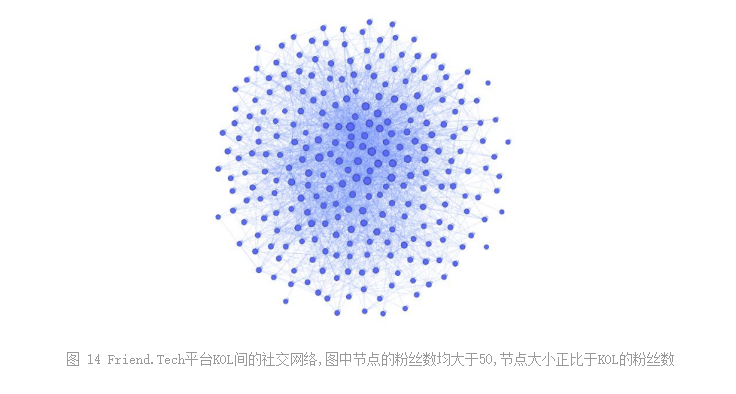

3.6 – User-to-User Social Network

Beyond finance, Friend.Tech remains a social platform. From Key ownership relationships, 110,000 out of 140,000 users (79.2%) form a single connected community—linked via mutual friends. While average friend count is small (~3–4 friends), connections are dense: ~41.3% of friends of friends are also friends—far higher than any existing social platform.

Additionally, we observe reciprocal behavior—users buying each other’s Keys. Though technically redundant to establish dual chat channels, this strengthens social ties. 13.5% of social relationships are reciprocal.

Figure 14 - The social network among platform KOLs, where each node represents a KOL with more than 50 followers, and the size of each node is proportional to the number of followers.

Figure 14 - The social network among platform KOLs, where each node represents a KOL with more than 50 followers, and the size of each node is proportional to the number of followers.4. Summary and Outlook

4.1 – Application Deficiencies

Currently in its early stage, Friend.Tech's core social features are relatively simple, lacking compelling retention mechanisms. Lack of verification allows impersonation (e.g., fake Twitter accounts like @punk9O95 mimicking @punk9059), frequent connectivity issues, message delays, and app crashes hinder usability.

Due to blockchain's openness, users can bypass the front-end and interact directly with the smart contract—for instance, generating Keys without linking a Twitter account. This undermines Friend.Tech’s original intent of promoting socialization through influence tokenization and weakens the effectiveness of the token economy.

Moreover, public API access to Twitter-X address bindings raises concerns about privacy in decentralized social products.

While these issues are expected during testing, and can likely be resolved by competent teams, what’s more concerning is Friend.Tech’s low barrier to entry. This became evident when the project tried to block cross-platform interaction for airdrop eligibility—an unpopular move that was eventually retracted on August 29 amid strong backlash. The founder admitted the action was driven by fear and zero-sum thinking, revealing Friend.Tech’s vulnerability in the SocialFi landscape—intense homogenized competition lies ahead.

4.2 – Web3-Powered Social Networking

Eurybia believes Web3’s long-term success hinges on attracting and retaining users unaffected by token speculation. According to Maslow’s hierarchy of needs, areas like daily life, employment, health, and emotional belonging are full of potential—but also uncertainty.

Rebuilding a social network is no easy task. Compared to other products, switching costs for users are extremely high. Simply luring users away from existing platforms isn't enough—their entire social circle must migrate too. In the Web2 era, few new platforms have successfully challenged incumbents—Google+ and Clubhouse serve as silent witnesses.

Yet Web3 brings unique advantages—token incentives provide the most direct and explicit customer acquisition mechanism.

Attracting 260,000 users in a month is already a remarkable feat for Friend.Tech. However, current Web3 social platforms suffer from flawed tokenomics and inflexible smart contracts, negatively impacting long-term viability.

We assess Friend.Tech’s current economic model as unsustainable. Although Key prices may remain stable despite reduced trading, decreasing volume threatens profitability for both the platform and KOLs. At least until a mature peer-to-peer Key market emerges, token appreciation as a growth driver has clear limits. Community initiatives like airdrop points aim to mitigate this issue.

Web3 projects typically attract speculators and investors via token airdrops, hype, and profit incentives. The challenge lies in converting these users into genuine users of the platform’s services (social, gaming, etc.). Generally speaking, compared to users interested in service content, speculators tend to care less about the actual product. If they capture most of the economic rewards but offer minimal loyalty, is token subsidy (if costly to the project) still justified? This is a critical question all Web3 mass-adoption advocates must deeply consider.